I Am a Quarter Millionaire: My Investing Strategy

In February 2026, my net worth (assets minus liabilities) surpassed $250,000. Ever since then, I have been building up the courage to make this post. I’ve never bought a lottery ticket before, but somehow I’ve convinced myself that when I win the lottery, I would accept my winnings anonymously and move to a remote, quiet island to live out my days.

So the thought of openly sharing what I, like many of you, have been so conditioned to keep close to the chest, is daunting. Though no one ever directly said it to me, I know that financial wins and shortcomings surely fall within the “dirty laundry” basket you keep at home.

But that is how we, as a community, stay poor. So, con miedo (with fear), here we go!

We are in a Financial Literacy Crisis

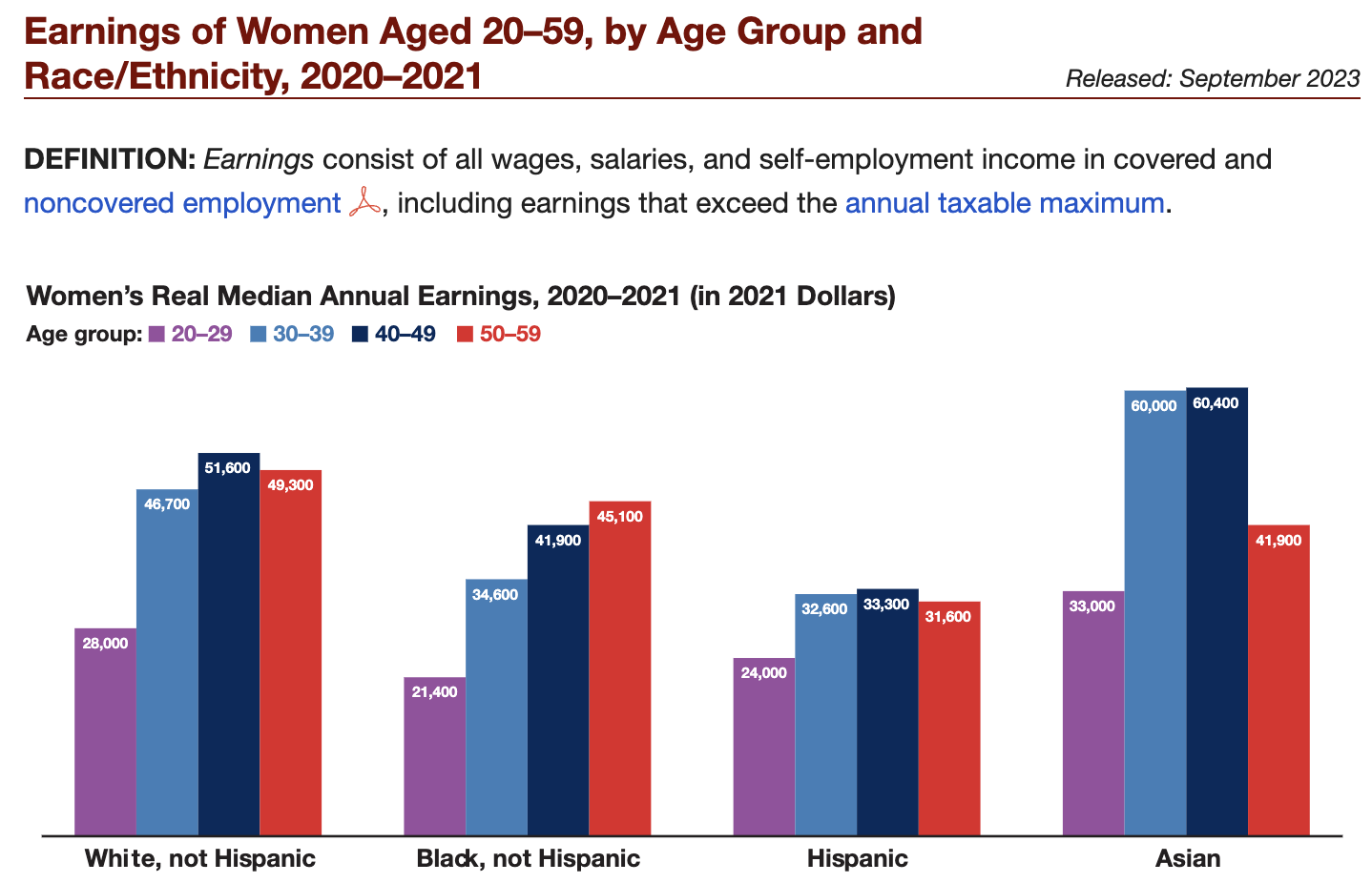

Financial literacy is not equally accessible, and the gaps disproportionately impact women of color.

According to the Pew Research Center, Americans in households with upper incomes (72%) are more likely than those in households with middle (56%) or lower incomes (42%) to say that they are knowledgeable about personal finances.

White adults (58%) are more likely than Black (50%) or Hispanic (41%) adults to say they know a fair amount about personal finance.

The Pew Research Center further found that 30% of women say they cannot pay some of their monthly bills. This compares with 21% of men.

Additionally, 43% of Black adults and 37% of Hispanic adults say they can’t pay some bills, while 23% of Asian adults and 19% of White adults say this.

Among income groups, 45% of lower-income Americans say they can’t pay some bills in a typical month. This compares with 19% of middle-income Americans and 7% of upper-income Americans.

Mix this in with the wealth gap for women of color (chart below) and you have a system that makes it incredibly challenging for Black and Hispanic women to build wealth.

My Mission

Financial literacy is not taught to us in high school, college, or even during advanced professional degrees. Instead, most people in the United States rely on their family and friends to develop their own financial literacy. But in Black and Brown communities we are simply not having these conversations because of deep shame and fear of judgment. The results are devastating:

In the United States, the median net worth for a head of family under 35 years old, is $39,040. This does not distinguish between race and gender, so women of color fall far below this number.

The hardest part of amassing a level of wealth that is too rare for women of color was not the financial jargon, the math, fancy Excel sheets, or excruciating working hours. The true challenges for me were the lack of access to relatable financial literacy and dealing with the guilt of having too much or not giving enough.

Relatable Financial Literacy

As a BigLaw attorney, not a week goes by without a fancy finance bro pitching his services to manage my investment portfolio. Yet, none of them look like me and frankly, many give off scammy vibes.

I graduated law school with over $220,000 in debt and a multiple-six-figure salary. By this point in my life, I knew I was objectively smart. I had the degrees, the honors, and the fancy job and accolades to prove it. And still, I felt clueless when it came to managing my money. As I started talking about money with my friends and family, I realized that many of us were in the same boat, so @k_the_scholar was born. Through these efforts, I have built a community that has watched me pay off my debt and build a solid financial foundation—in real time.

I know it is cliché to say, but if I can do it, you can do it too. I mean that.

As I reflect back on the different versions of myself, I hold so much grace for the younger version of me who had to navigate foster care, college, law school, and the corporate world with little guidance. I hold grace for the version of myself that held so much shame about my family’s financial instability. The version of me that would stay up until dawn dreaming, planning, and strategizing for the life that I now have.

So regardless of your starting point—you truly can do it too.

Dealing with Survivor’s Guilt

My personal finance journey has required working through the guilt of putting my needs over those of my parents, extended family members, or even strangers online. This has not been easy.

In making this post, this is where most of my fear lives. The fear is not about the wide internet learning about little ol’ me. The fear is what distant family and friends would think about me. Those family and friends who do not have frequent access to me, but who are connected to me by forces larger than me. I know they will have opinions about my “hunger” for money and will certainly have many thoughts on how my money would be better spent. Surely, there is someone going through something, and I should be showing up for them because that’s what family does. That’s what community does.

But even greater than my responsibility to my community, is my responsibility to myself and to my children.

As I reflected on this fear, I realized that in many ways I have been facing this fear for years. I have been politely defying my family's expectations of me my entire life. Throughout my life I’ve walked around as both the black sheep and the shining star of my family. So here is where I landed on this fear:

I love my family and community. I have a responsibility to pour into my community and I live out this responsibility daily. I give abundantly, but I do so on my own terms and in ways that will not derail my dreams.

So I encourage you to do the same. Set and enforce boundaries. Advocate for yourself and your nuclear family. Challenge yourself and you can achieve the unimaginable—even if means being a little defiant.

My Real Numbers

The key to building wealth is consistency and time in the market. With this in mind, I have automated all of my accounts creating an investment system that takes me less than 15 minutes a month to manage.

So here is a breakdown of my net worth. The strategy is quite boring:

$180,000 in 401(k)s

$50,000 in HYSA

$8,000 in a brokerage account

$7,000 in 529 plans

$5,000 in crypto

Here are the accounts I invest in:

401K Retirement Accounts

A 401(k)is one of the most common ways people invest for retirement, especially if they work for a company. This is a long-term investment account that your employer often helps you fund. Generally, money is automatically taken out of your paycheck and invested—usually in mutual funds or index funds—so it can grow over time.

One of the biggest perks? Many employers offer a company match. For example, if you contribute 5% of your salary, your employer might match part or all of that contribution. That’s essentially free money toward your retirement.

Another benefit is the tax advantage. With a traditional 401(k), the money you contribute is taken out before taxes, which can lower your taxable income today.

The trade-off is that the money is meant to stay invested until retirement. If you withdraw it early, you’ll usually face taxes and penalties though many exceptions exist.

High-Yield Savings Account

An HYSAis a savings account that pays a much higher interest rate than a traditional bank account. These accounts are usually offered by online banks and are great for things like:

Emergency funds (3-6 months of living expenses)

Short-term savings goals

Money you may need in the near future

Unlike investing accounts, the money isn’t exposed to market ups and downs. It’s designed to be stable and easily accessible.

The trade-off is that while the interest is higher than a normal savings account, the growth is usually slower than what you might get from long-term investing in the stock market.

Think of a high-yield savings account as the safe parking spot for money you want to protect while still earning something on it.

Brokerage Account

A brokerage account is the most flexible investment account available. This is where you can buy and sell investments like:

Stocks

ETFs (exchange-traded funds)

Bonds

Mutual funds

Unlike retirement accounts, brokerage accounts don’t have strict rules about when you can withdraw money. You can invest, sell, and access your funds whenever you want.

The trade-off is taxes. Because brokerage accounts don’t have the same tax advantages as retirement accounts, you may owe taxes on investment gains and dividends.

Still, brokerage accounts are often the go-to tool for people who want to grow wealth beyond retirement accounts. You can think of it as your general-purpose investing account.

529 Education Investment Plans

A 529 plan is an investment account designed specifically for education savings.

Parents, grandparents, and family friends can contribute to one, and the money grows tax-free as long as it’s used for qualified education expenses. That includes things like tuition, books, housing, and sometimes even K–12 tuition.

The idea is similar to a retirement account, but the goal is funding a child’s education instead of retirement.

One nice feature is flexibility. If the child you originally saved for doesn’t use all the money, you can often transfer the account to another family member.

Cryptocurrency

Cryptocurrency is a newer type of digital asset that exists on blockchain technology rather than through traditional banks or financial institutions.

Popular examples include Bitcoin and Ethereum, but there are thousands of different cryptocurrencies.

Unlike stocks, cryptocurrencies don’t represent ownership in a company. Instead, they’re digital assets whose value is driven by supply, demand, and adoption.

Some people view crypto as:

A speculative investment, known for extreme price volatility. Values can rise dramatically—and fall just as quickly.

A hedge against traditional financial systems

A technology with long-term potential

Because of that, cryptocurrency should be treated as a small, higher-risk portion of a broader investment strategy, rather than the core of a portfolio.

That’s it.

With that, I wish you all wealth!