How My Grandma Taught Me to Build Perfect Credit - A Beginner-Friendly Guide To Credit Scores

Let me take you back to the beginning of my adult financial history. I arrived in Hartford, Connecticut a few days after my 18th birthday. In my wallet: $175 cash, a college checking account with an additional $100, and my newly minted student ID that gave me access to the opulence that was pouring from every corner of my college campus.

Shortly after arriving, I learned that my bank–which held about a third of my life’s savings–did not have a location anywhere near my new hometown. By this time, as is my nerdy nature, I had already bonded with a college dean over our shared name. I remember walking into her office and politely asking about nearby banks and how to go about opening an account.

Without hesitation, she paused her work day to drive me to the local bank. After coaching me through the script I was to recite to the bank teller, she sat in the parking lot on a hot Connecticut day patiently waiting for me to emerge with the newest addition to my wallet: a local debit card.

Months later, I needed airfare to go home for the holidays and getting a credit card was as easy as filling out a single page on a clipboard as I waited in line at the cafeteria.

With that, my credit journey began.

But the foundation had already been laid years earlier. My grandma had always instilled in me the value of being a “Gallinita Ahorradora” (a saving chicken lol) so early on I knew that it was important to save my money and pay my bills on time.

I didn’t realize it then, but that simple philosophy became my financial superpower. I built a strong credit history early—not because I was financially sophisticated, but because I was consistent.

Still, like many of us, I wasn’t immune to credit traps.

My next credit card was a Victoria’s Secret credit card that I had no business having, but the young version of me felt that the body mist specials were just too good to pass up. A year and thousands of dollars later, it hit me how silly and unnecessary this card was and I closed the account.

That was my first real lesson: credit isn’t just access—it’s temptation if you don’t understand it.

Fast forward to today and my credit history is much more complex: student loans, personal loans, credit cards, and credit lines.

And yet, one thing remains true:

I’ve always had near-perfect credit thanks to my grandma’s lessons: “Always save for a rainy day and if you want people to respect you–pay them back.”

Do you remember getting your first credit card? If your story resembles mine and your credit knowledge stops at whatever you learned from uninformed friends, at a college fair, or at your favorite store at the mall, then it is time to change that.

Credit isn’t just about borrowing money—it’s about access. It impacts where you live, the interest rates you pay, and even certain job opportunities. Understanding how credit works is one of the most powerful steps you can take toward building wealth and creating options for your future.

So let’s dive in.

What is a Credit Score?

Your credit score is your financial reputation—it’s a three-digit number that tells lenders how trustworthy you are with money. Think of it as your “grade” as a borrower.

Scores typically range from 300 to 850, and the higher your score, the better. A strong credit score can help you:

Get approved for apartments, mortgages, personal loans, and credit cards

Qualify for lower interest rates

Save thousands of dollars over time

How is Your Credit Score Calculated?

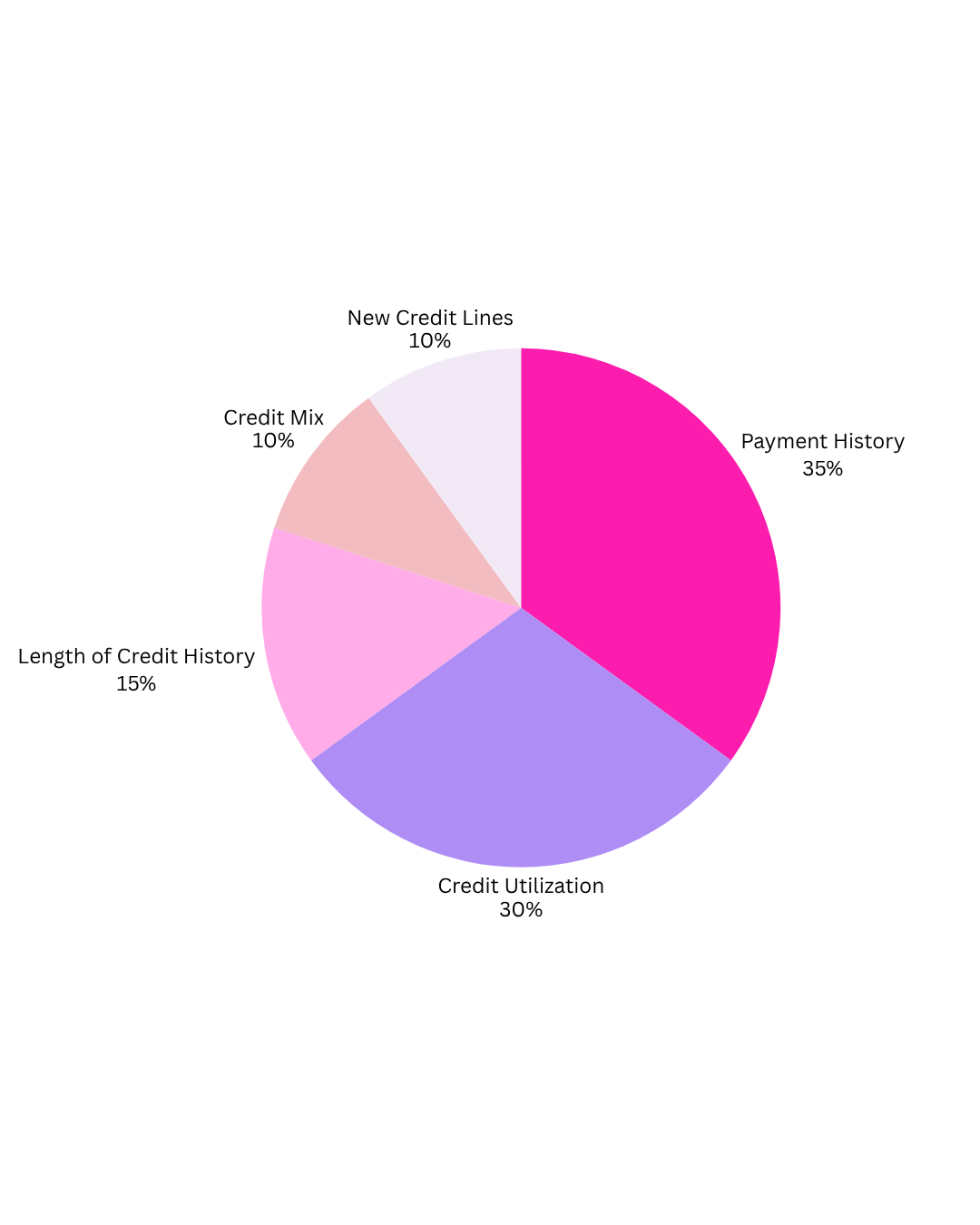

Your credit score is based on five key factors. Once you understand these, you can start improving your score strategically:

Factors that make up your credit score.

Payment History (Most Important). Do you pay your bills on time? Even one missed payment can hurt your score. Consistency is key and setting automatic payments can be a game changer.

Credit Utilization. This is how much of your available credit you’re using. Aim to pay your credit card bills in full each month and keep all lines of credit below 30%. For example, if you have a credit limit of $1,000 you should never carry a balance greater than $300.

Length of Credit History The longer your credit history, the better. Time matters here—so start building early and stay consistent.

Credit Mix. Having a mix of credit types (like credit cards and loans) shows lenders you can handle different kinds of debt responsibly.

New Credit. Opening too many accounts in a short time can lower your score. Be intentional about when and why you apply.

Why Credit Matters (More Than You Think)

Good credit isn’t just about loans—it’s about freedom and opportunity.

With strong credit, you can:

Secure better housing options

Pay less in interest (keeping more money in your pocket)

Access funding to start a business

Handle emergencies without financial panic

In short: good credit gives you options—and options are power.

How to Start Building (or Improving) Your Credit

If you’re starting from scratch or rebuilding, here are simple, effective steps:

Check Your Credit Report Review your reports from Equifax, Experian, and TransUnion for errors. Fixing mistakes can boost your score quickly.

Pay Everything on Time Set reminders or autopay—this is the #1 factor in your score.

Keep Balances Low Try not to max out your cards. Lower balances = higher scores.

Be Strategic About New Credit Only apply when necessary. Every hard inquiry matters.

Build Credit Intentionally

Become an authorized user on a trusted person’s card

Open a secured credit card to get started

Tackle Debt with a Plan Focus on paying down high-interest debt first to free up your money faster.

Your credit score is a key part of your money story—but it doesn’t define you. It’s a tool you can learn, improve, and leverage.

By understanding how credit works, you’re not just building a score—you’re building financial confidence, stability, and generational wealth.

Wishing you all the wealth ✨

Make sure to subscribe so you don’t miss the next bi-weekly post.